-

Wishing you a healthy and prosperous Year of the Ox 新春愉快, 吉祥如意

2020, the Year of the White Metal Rat, proved to be an unexpectedly challenging year in every respect. Life disrupted. Travel virtually ceased. Health and safety prioritised.

It also was the year The Lantau Group turned 10. It was a most extraordinary and transformative year in which we laid a strong foundation for our future. As we prepare for Year of the White Metal Ox in 2021, we wanted to take a moment to share some of our experiences.

It was an important year to embrace the Rat’s strengths: its insightfulness, adaptability, curiosity, and assiduous hard work. We focussed on expanding our market coverage, regional depth, and our team. Most importantly we worked even more closely together, despite being spread across locations throughout the region. All of us, young and old(er), rose to new challenges in our unique ways. Equally, we avoided the Rat’s short-sightedness and indecision; instead acting on opportunity and investing in our future purposefully and strategically.

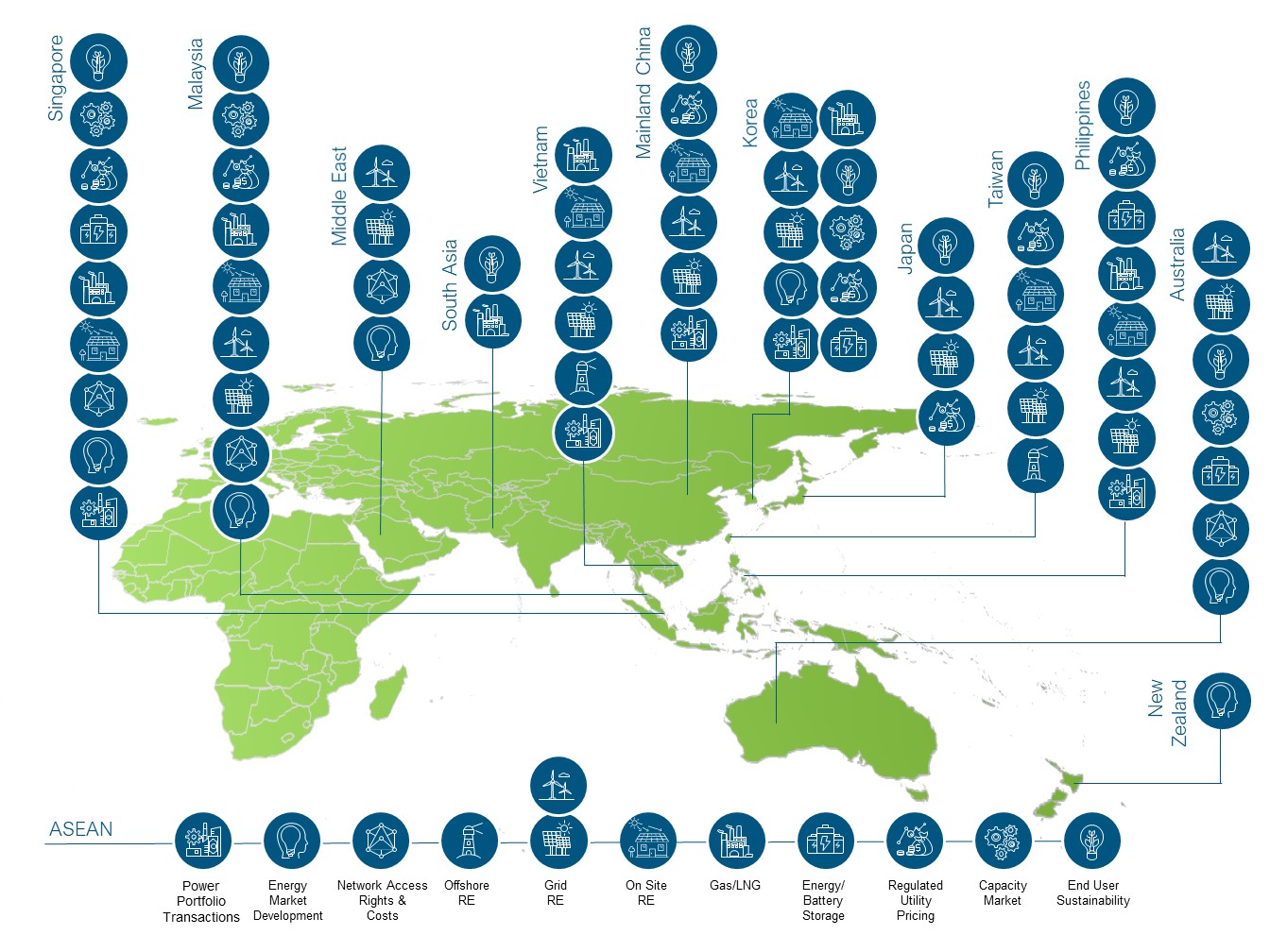

One thing that really stood out about 2020 was how the energy sector continued – and arguably accelerated – its dramatic transformation throughout the region. We undertook projects for clients in more than 20 markets, including in Southeast and Northeast Asia, South Asia, China, Australia, and New Zealand. We also continued our work in select Middle East markets, with team members in Abu Dhabi and Riyadh and projects in Oman.

A growth area has been the end-user side of the renewables business. We combined traditional market and regulatory insights in each of the markets in the region, including market modelling, with our long-standing work on retail electricity and gas tariff trends that we have generally done for industrial clients. We leveraged that to support developers and end-users looking at new opportunities in different markets around the region in terms of corporate PPAs and green power sourcing and supply. Corporate entry into the energy sector is the beginning of a transformative trend that will also reshape regulation, policy, the role of incumbent power companies, and market design.

In terms of geographic markets, TLG’s original focus markets in Southeast Asia, such as the Philippines, Vietnam, Malaysia, and Singapore, continued to be as active and dynamic as ever across a very wide spectrum of commercial, regulatory, and strategy engagements. But we were both pleased and even surprised by the extent to which the energy sector in China has become more innovative and dynamic. It’s well known that the Chinese market is incomparable in sheer size. But what is less commonly known is the multitude of regulatory changes currently liberalising both wholesale markets and supply to corporate end-users. China’s power sector is quickly becoming more diverse and complex — in good and necessary ways.

We were also very pleased to see the business momentum we have created in the Australian market, exemplified by the opening of our first local office and the establishment of a TLG presence in both Western Australia and the eastern-based National Electricity Market. And looking into TLG opportunities further abroad and into the future, we followed our clients into Japan. Here we established a local team focussed on renewable energy and market modelling for commercial end-users and investors.

Best wishes for a healthy, happy, and prosperous Year of the White Metal Ox. This is a year rewarding hard work. Strong and reliable, the Ox inspires others. We’re determined to continue to embody its spirit and demonstrate these traits to the benefit of our clients and ourselves.

We take a somewhat deeper look at our regional activity below.

More Offices, More People

We strengthened our management team and extended our consulting team bench strength. All in all, 10 new staff joined us at TLG, and at every level of TLG. It wasn’t planned, but 2020 proved to be the most transformative in our history – whether because of the pandemic, or in spite of it.

- We expanded our capabilities for natural gas and LNG stakeholders through our expert senior advisor Tony Taylor, team lead Lee Shir Heng, and manager Wendy Yong, especially in the areas of LNG procurement and contracting. Our gas team in conjunction with our economics team have exceptional experience in third party access to gas infrastructure and gas market liberalisation.

- We welcomed David Kim as a Partner and Director. With a background in renewable energy and business strategy he led the opening of our Seoul office. TLG Korea advises on strategy and opportunities in energy inside and outside of South Korea with a contact network among Korea chaebols and energy market stakeholders.

- We elevated Chris Starling to Partner and Director. Chris has particular experience across the Philippines, Thailand, and Vietnam, having directed and managed numerous engagements for IPPs, developers and investors, involving LNG/gas-to-power project assessments, upstream gas monetisation, and commercial advisory across conventional and renewable energy, including ‘behind-the-meter’ distributed solutions.

- We welcomed Dr David Broadstock, who took up a board member position and added his immense expertise in advanced analytics to the TLG portfolio. Perhaps nothing defines TLG’s belief in the future more than our commitment to deeper analytics as the underpinning of the new energy transformation.

- We formed our in-house deep analytics resources and tools (DART) team, led by Paul Buckland, to maintain, extend, and develop our models, challenge our thinking about methods, and enable our ability to access, manage, and analyse vast amounts of data covering everything from fuel markets to all of the region’s electricity sectors.

- We welcomed Ian Benfield as a senior advisor. The core of Ian’s experience derives from the developing competitive UK gas and electricity markets in the 1990s. This has been supplemented by a subsequent 17 years’ in a range of emerging markets across most the world, specifically in Europe, Asia, Africa, and the Middle East. He also sat as Director of the Authority for Electricity Regulation in Oman for a decade.

- We welcomed Colin Tam as a senior advisor. Colin has over 44 years of experience in USA, Asia, and Middle East as an entrepreneur and senior executive. He is now a developer, strategic advisor, and investor in the following industries: renewable energy, Fintech, emerging environmental related technologies. He maintains an extensive network in the related business, government, and financial sectors. Colin was a founder and CEO of two successful regional energy companies which are now listed on the HK Stock Exchange by their new owners. He is the current chairman of 2 NGOs, HAESCO and IPPF.

As the new year of the White Metal Ox begins, we combine our hard work with a clear focus on helping our clients meet the challenges of the energy transformation. 2021 also promises to be the year we launch new publication/subscription options for those interested in deeper divers on specific issues or general periodic coverage of key markets. Relatedly, we will soon be publishing our first premium industry report, prepared with Tecnon OrbiChem, on China’s Chlor Alkali sector – a sector for which power is a key cost input. Over time, we will look at other highly electricity intensive sectors and for similarly exceptional specialist partners with whom to develop insightful studies for our clients.

Regionally, our work expanded in multiple countries and dimensions.

Northeast Asia

Our work in Northeast Asia has grown steadily, driven by the twin pillars of natural gas and renewable energy. Some highlights:

Japan – We took the leap and added on-the-ground, in-country expertise in Japan, through a prior client and renewable energy expert, Shintaro Doi. The impact was immediate given the strong interest in corporates for renewable energy options and the challenges they face in Japan’s complex market. We are also preparing our Japan electricity market model roll-out for early 2021 to assist our clients with the insights they need to make better decisions about opportunities in the sector, including off-shore wind.

Korea – Based on growing interest in Korean renewables and general electricity markets, especially since 2018, we opened our Seoul office, with a team of David Kim, Soyeon Park, Tina Cui, and Minji Kim. We continue our work with large end users and sector stakeholders, allowing us to even better support domestic and international clients looking at the opportunities in the Korean renewable energy and energy technology sectors. In particular, we used our in-house modelling tools to advise on the outlook for Korea’s Renewable Energy Credit (REC) market and its energy market. We also advised on a major district heating and cooling project, the viability of new fuel cell project, and on several major LNG opportunities being developed or contemplated by our Korean clients throughout the region.

Mainland China – We continued building the foundations for our upcoming Shanghai office, which we expect to launch in 2021. In China, we’ve seen steady interest in renewable energy development behind the meter and on-grid. And after many years of tracking and analysing tariff formation for end users, we are applying our insights to assist renewable energy developers evaluate behind the meter solar opportunities. In collaboration with several stakeholders, work began on a provincial power dispatch model.

Taiwan – We continued to advise multiple generation developers and financial stakeholders on opportunities off and on-shore and advised end users on energy costs and renewable energy contracting opportunities. In 2020, the market focus shifted even more strongly to offshore wind with some of the region’s most dramatic project announcements. The corporate PPA space is also becoming more active as global supply chains face greater pressures to ‘go green’ over the next decade and beyond.

Southeast Asia

We grew our regulatory and commercial work throughout ASEAN. In the area of regulatory economics, we expanded our work on tariffs, cost of service, wholesale market development, third party access, and performance-based regulation. In the fast moving commercial and industrial end user energy and rooftop solar space, we played an integral role advising some of the key regional rooftop solar/C&I energy and services transactions/investments, supporting Olympus Capital Asia’s investment into Constant Energy and Norfund-KLP’s investment into BECIS. We also supported the development of a debt platform for one of SE Asia’s largest rooftop solar players. All of this was additional to our extensive strategy and analytics work for stakeholders looking at transactions or future directions. Some other highlights:

Vietnam – The astonishing developments across the Vietnam market are no fluke, as they accelerated throughout 2020 and are continuing in 2021. Vietnam kept Covid-19 under control with almost the fewest cases of any country anywhere in the world, and certainly of a major emerging market. Benefitting as well from supply chain interest in diversifying in the region, Vietnam has continued to impress as an energy sector focus area:

- We worked on over ten assignments ranging from monetisation of domestic gas, to LNG sourcing and procurement for a new LNG terminal;

- We were engaged for market analysis, due diligence, and transaction support for multiple M&A deals or market entry strategies including one for a domestic coal-fired project selling power into the VWEM, and another for a small hydro power project, and yet more in the solar and wind sectors, including both rooftop solar and offshore wind;

- We developed forecasts of wholesale and end-user retail tariffs for developers looking at the rapidly expanding behind-the-meter sector as well as corporate PPAs;

- We contributed to ADB’s detailed country Assessment, Strategy, and Roadmap (ASR) publications for Vietnam and Thailand, building on our previous support for their activities in Laos and the Philippines.

By the end of 2020, there were few aspects of Vietnam’s electricity and gas/LNG markets that we had not covered in some way or another.

The Philippines – We have been steadily engaged with our clients in the Philippine energy sector since 2007. Over that time, we have worked across virtually all aspects of the Philippine energy sector from regulation, commercial activity, and business strategy. Using our modelling suite and deep sector knowledge, we have had the opportunity to advise on virtually all major transactions either on the buy- or sell-side. Some other observations include:

- As the WESM grows and evolves, so does our work. This extends to advisory support on transactions involving new LNG and gas opportunities, renewable energy and batter storage developments on both sides of the meter, as well as the complicated outlook for conventional power.

- The internationalisation and general rebalancing of the energy sector continues, with several Philippine energy stakeholders pursuing overseas investment opportunities elsewhere in TLG markets throughout Asia, even as new international stakeholders demonstrate their interest in the Philippines. In the acquisition/transaction space, we worked with EY on GIC’s PhP20 billion investment into AC Energy Philippines; assisted an infrastructure investment manager divesting its stake in a large coal fired IPP; and advised another international client on its divestment of a diverse portfolio of hydro assets.

Malaysia and Singapore – Members of our team have worked on energy sector engagements in both Malaysia and Singapore since the late 1990s. We have a deep understanding of these crucial energy markets and their respective challenges and opportunities. More specifically:

- In 2020 we continued our work in Malaysia, undertaking multiple extensive studies. These examined improving gas sector third party access functionality, cost of service, tariff design, and incentive-based regulation, another on tariff benchmarking and end user price projections for datacentres and industrial users corporate green energy contracting, and wheeling charge development.

- In Singapore, we saw a strong uptick in commercial interest as excess gas challenges are reducing and demand growth is picking up. Even so, there remains many challenges ahead. Our work has included assessing the impact of solar integration, advising on-site solar procurement, possible power import opportunities, and analysing the proposed forward capacity market in detail for many stakeholders. One of the most interesting developments for the future is the scope for use or even expansion of the electricity interconnection between Malaysia and Singapore and how that could impact both markets.

South Asia and Middle East

TLG’s latest frontier has been to the west, and in 2020 we continued our expedition. South Asian markets are becoming increasingly important to our clients. We also continued our work in Oman, which, as a relatively smaller, but very dynamic market, shares many of the same challenges and opportunities as many of the smaller electricity and gas markets we work in throughout Asia.

Our South Asia work has been centred around two areas: one is (of course) renewable energy, with India a global leader, with our work in 2020 encompassing both batteries and corporate green energy options, and where Bangladesh and Pakistan (in our view) now look poised to see a significant ramping up in renewable energy in near or medium term. The other main area of our work has been in LNG and gas-fired generation, where TLG’s two-legged expertise in power and gas/LNG has been fitting when looking at the intersection of upstream and downstream gas-to-power projects. In 2020, we boosted our execution capacity for South Asia in several ways. We refined our models for the electricity markets in Bangladesh and Pakistan. There was also the appointment of new people well experience in the Pakistan LNG sector, complementing our already strong track record in LNG related projects in Bangladesh. We established strategic relationships with very strong locally based energy experts in all three markets of India, Pakistan, and Bangladesh.In 2020, our work in Oman focussed on direct sales (corporate PPAs) and the scarcity pricing mechanism, each building on prior work on retail choice and on potential unintended consequences of aspects of the incentive regulatory framework. With the addition of Ian Benfield (see below “Laying our Foundation”) to our regulatory economics team, we took a big step forward in strengthening our capabilities across the region, particularly with respect to the challenges of smaller, dynamic, energy markets. By end of 2020 we had TLG staff and/or Senior Advisors on the ground in Riyadh and Abu Dhabi.

Australia and New ZealandThe competitive energy markets in Australia and New Zealand are amongst the most advanced in the world, with many insights arising from their maturation and evolution over the past three decades. Some of us started working on energy sector reforms in New Zealand as early as 1989, deep in the era of fax machines, acetates, Lotus 1-2-3, and very long-distance telephone calls – well before modern email or the now ubiquitous Microsoft Excel and PowerPoint. Electricity spot markets were new concepts heralding untold possibilities of fundamental changes to the vertically integrated utility.

In 2020, we opened our Perth office to support our growing work in both Western Australia and the country’s Eastern Seaboard. We were engaged to advise on key parts of the WA Government’s wide-ranging energy market reforms, extending on our prior work on the reserve capacity mechanism, with a particular focus on transitioning the capacity market to operate within a constrained network framework and allowing for battery storage capacity to participate.

While battery storage integration in capacity markets was one major theme, we also tackled more strategic questions around opportunities for batteries versus other technologies to provide longer duration storage or otherwise contribute profitably to maintaining reliability. Another area of common interest in both countries was the framework for pricing and investment in transmission. New Zealand’s transmission pricing methodology – an area on which we have long advised -- has been debated and contested for over a decade. New Zealand is set to head in a challenging direction as it moves to put a more complex economic framework for transmission pricing in place. The prospect of rising tension between theory and practice will something to watch.

Despite the pandemic, 2020 was a busy, fulfilling year in which several major forces driving the energy sector accelerated their impact. We are immensely grateful for our terrific team and invaluable clients — you make it all possible.